![Ways To Overcome Affordability Challenges in Today’s Housing Market [INFOGRAPHIC] Simplifying The Market](https://files.keepingcurrentmatters.com/content/images/20230428/Ways-To-Overcome-Affordability-Challenges-In-Todays-Market-KCM-Share.png)

Some Highlights

- With so few homes on the market right now, widening the scope of your search to include nearby areas could help you find more options in your budget.

- You can also work with a trusted lender to consider alternative financing options and search for down payment assistance.

- If you’ve been searching for a home but are concerned about rising costs, make sure you have a team of trusted real estate professionals for expert advice.

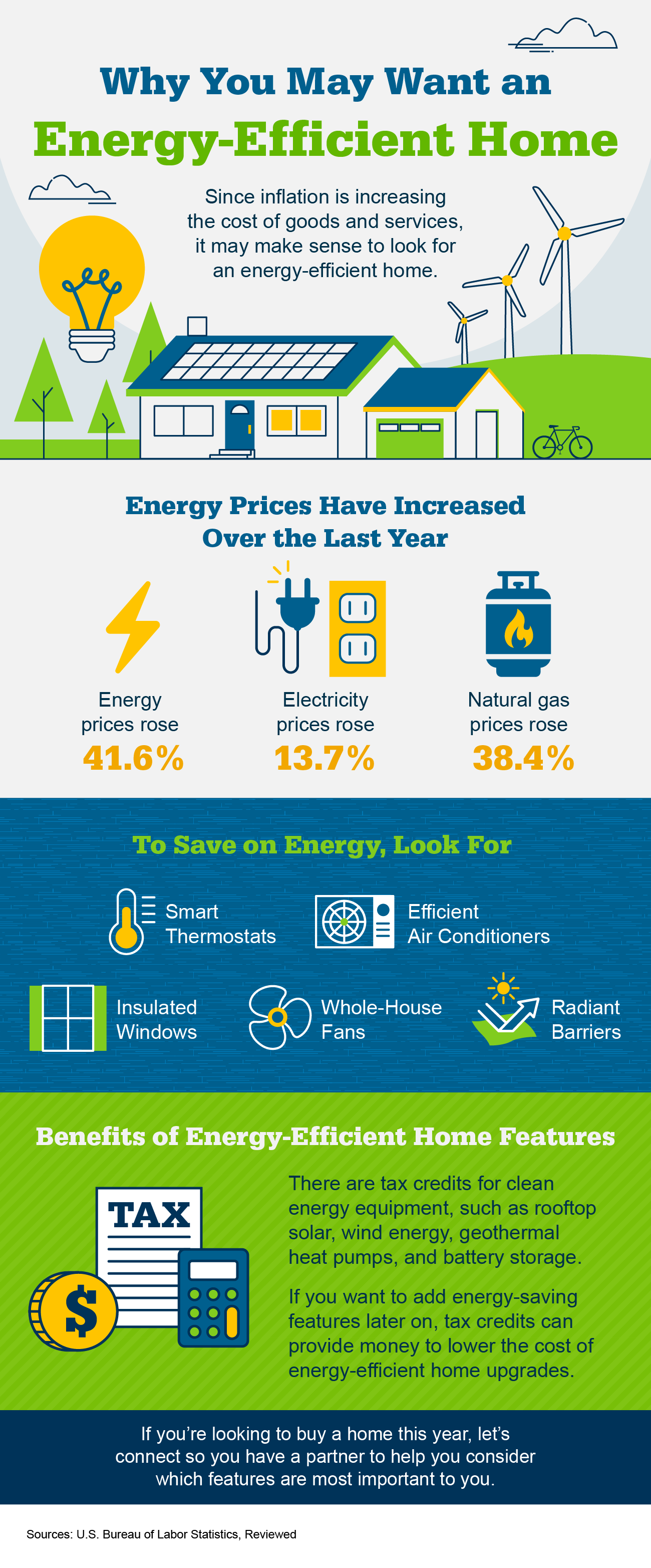

![Why You May Want an Energy-Efficient Home [INFOGRAPHIC] Simplifying The Market](https://files.keepingcurrentmatters.com/content/images/20230420/Why-You-May-Want-An-Energy-Efficient-Home-KCM-Share.png)