With higher mortgage rates and moderating buyer demand, conditions in the housing market are different today. And if you’re thinking of selling your house, it’s important to understand how the market has changed and what that means for you. The best way to make sure you’re in the know is to work with a trusted housing market expert.

Here are five reasons working with a professional can ensure you’ll get the most out of your sale.

Leslie Rouda Smith, 2022 President of the National Association of Realtors (NAR), explains:

“During challenging and changing market conditions, one thing that’s calming and constant is the assurance that comes from a Realtor® being in your corner through every step of the home transaction. Consumers can rely on Realtors®’ unmatched work ethic, trusted guidance and objectivity to help manage the complexities associated with the home buying and selling process.”

An expert real estate advisor has the latest information about national trends and your local area too. More importantly, they’ll know what all of this means for you so they’ll be able to help you make a decision based on trustworthy, data-bound information.

Home price appreciation has moderated this year. If you sell your house on your own, you may be more likely to overshoot your asking price because you’re not as aware of where prices are today. If you do, you run the risk of deterring buyers or seeing your house sit on the market for longer.

Real estate professionals provide an unbiased eye when they help you determine a price for your house. They’ll use a variety of factors, like the condition of your home and any upgrades you’ve made, and compare your house to recently sold homes in your area to find the best price for today’s market. These steps are key to making sure it’s set to move as quickly as possible.

Since buyer demand has cooled this year, you’ll want to do what you can to help bring in more buyers. Real estate professionals have a large variety of tools at their disposal, such as social media followers, agency resources, and the Multiple Listing Service (MLS) to ensure your house gets in front of people looking to make a purchase. Investopedia explains why it’s risky to sell on your own without the network an agent provides:

“You don’t have relationships with clients, other agents, or a real estate agency to bring the largest pool of potential buyers to your home.”

Without access to the tools and your agent’s marketing expertise, your buyer pool – and your home’s selling potential – is limited.

Today, more disclosures and regulations are mandatory when selling a house. That means the number of legal documents you’ll need to juggle is growing. NAR explains it like this:

“Selling a home typically requires a variety of forms, reports, disclosures, and other legal and financial documents. . . . Also, there’s a lot of jargon involved in a real estate transaction; you want to work with a professional who can speak the language.”

A real estate professional knows exactly what all the fine print means and how to work through it efficiently. They’ll help you review the documents and avoid any costly missteps that could occur if you try to handle them on your own.

In today’s market, buyers are also regaining some negotiation power as bidding wars ease. If you sell without a professional, you’ll also be responsible for any back-and-forth. That means you’ll have to coordinate with:

Instead of going toe-to-toe with all the above parties alone, lean on an expert. They’ll know what levers to pull, how to address everyone’s concerns, and when you may want to get a second opinion.

Don’t go at it alone. If you’re planning to sell your house this winter, let’s connect so you have an expert by your side to guide you in today’s market.

While it’s exciting to start thinking about moving in and decorating after you’ve applied for your mortgage, there are some key things to keep in mind before you close. Here’s a list of things you may not realize you need to avoid after applying for your home loan.

Lenders need to source your money, and cash isn’t easily traceable. Before you deposit any amount of cash into your accounts, discuss the proper way to document your transactions with your loan officer.

It’s not just home-related purchases that could disqualify you from your loan. Any large purchases can be red flags for lenders. People with new debt have higher debt-to-income ratios (how much debt you have compared to your monthly income). Since higher ratios make for riskier loans, borrowers may no longer qualify for their mortgage. Resist the temptation to make any large purchases, even for furniture or appliances.

When you cosign for a loan, you’re making yourself accountable for that loan’s success and repayment. With that obligation comes higher debt-to-income ratios as well. Even if you promise you won’t be the one making the payments, your lender will have to count the payments against you.

Lenders need to source and track your assets. That task is much easier when there’s consistency among your accounts. Before you transfer any money, speak with your loan officer.

It doesn’t matter whether it’s a new credit card or a new car, when you have your credit report run by organizations in multiple financial channels (mortgage, credit card, auto, etc.), it will have an impact on your FICO® score. Lower credit scores can determine your interest rate and possibly even your eligibility for approval.

Many buyers believe having less available credit makes them less risky and more likely to be approved. This isn’t true. A major component of your score is your length and depth of credit history (as opposed to just your payment history) and your total usage of credit as a percentage of available credit. Closing accounts has a negative impact on both of those aspects of your score.

Be upfront about any changes that occur or you’re expecting to occur when talking with your lender. Blips in income, assets or credit should be reviewed and executed in a way that ensures your home loan can still be approved. If your job or employment status has changed recently, share that with your lender as well. Ultimately, it’s best to fully disclose and discuss your intentions with your loan officer before you do anything financial in nature.

You want your home purchase to go as smoothly as possible. Remember, before you make any large purchases, move your money around, or make major life changes, be sure to consult your lender – someone who’s qualified to explain how your financial decisions may impact your home loan.

If you’re thinking about buying or selling a home, you probably want to know what’s really happening with home prices, mortgage rates, housing supply, and more. That’s not an easy task considering how sensationalized headlines are today. Jay Thompson, Real Estate Industry Consultant, explains:

“Housing market headlines are everywhere. Many are quite sensational, ending with exclamation points or predicting impending doom for the industry. Clickbait, the sensationalizing of headlines and content, has been an issue since the dawn of the internet, and housing news is not immune to it.”

Unfortunately, when information in the media isn’t clear, it can generate a lot of fear and uncertainty in the market. As Jason Lewris, Cofounder and Chief Data Officer at Parcl, says:

“In the absence of trustworthy, up-to-date information, real estate decisions are increasingly being driven by fear, uncertainty, and doubt.”

But it doesn’t have to be that way. Buying or selling a home is a big decision, and it should be one you feel confident making. To help you separate fact from fiction and get the answers you need, lean on a local real estate advisor.

A trusted expert is your best resource to understand what’s happening at the national and local levels. They’ll be able to debunk the headlines using data you can trust. And using their in-depth knowledge of the industry, they’ll provide context so you know how current trends compare to the normal ebbs and flows in the industry, historical data and more.

Then, to make sure you have the full picture, they’ll tell you if your local area is following the national trend or if they’re seeing something different in your market. Together, you’ll use all of that information to make the best possible decision for you.

After all, making a move is a potentially life-changing milestone. It should be something you feel ready for and excited about. And that’s where an agent comes in.

If you have questions about the headlines or what’s happening in the housing market today, let’s connect so you have expert insights and advice on your side.

Are you prepping to buy your first home? If so, one of the steps you should take early on is making sure you’re financially ready for your purchase. Here are just a few of the financial fundamentals you’ll need to focus on as you set out to buy a home.

Your credit is one element that helps determine which home loan you’ll qualify for. It also impacts your mortgage interest rate. While there are many factors that go into your mortgage application, a higher credit score could lead to a lower monthly payment in the long run.

So how do you make sure your credit is in the best shape possible when it’s time to buy? A recent article from NerdWallet lists a few tips you can use as you work to build and strengthen your credit. They include:

You might also be wondering how you can achieve your down payment savings goals. Bankrate provides buyers with a number of tips to help you save, including searching for down payment assistance programs and ways you can save more, faster. As the article says:

“One of the best ways to save for anything — including a down payment — is to set it and forget it. If you receive a regular paycheck, ask your employer to direct a portion of that payment into a savings account. If you’re a freelance worker or independent contractor, set up a recurring transfer from a checking account to a savings account to establish the routine.”

As you prepare for your purchase, you’ll also need to have a good grasp on your budget and how much you’ll be able to borrow for your home loan. That’s where the pre-approval process comes in.

Pre-approval from a lender lets you know how much money you can borrow for your home loan. And having that knowledge, plus an understanding of your savings, can help you decide on your target price range for a house.

From there, you can start browsing for houses online and see what’s available in your area in that general price point. This can help you really understand your options so you can start to picture your future home.

Finally, the best way to make you’re prepared for your purchase is to connect with trusted real estate professionals. Having expert advisors in the industry will help you make strong decisions throughout the homebuying process based on your specific goals, finances, and situation. They know the market and can guide you toward the home of your dreams.

If you’re ready to get the homebuying process started, let’s connect so you can begin to build your team of professionals today.

There’s no denying the long-term financial benefits of owning a home, but today’s housing market may have you wondering if now’s still the time to buy. While the financial aspects of buying a home are important, the non-financial and emotional reasons are too.

Home means something different to all of us. Whether it’s sharing memories with loved ones at the kitchen table or settling in to read a book in a favorite chair, the emotional connections to our homes can be just as important as the financial ones. Here are some of the things that make a house a home.

1. You Can Be Proud of Your Accomplishment

Buying a home is a major life milestone. Whether you’re setting out to buy your first home or your fifth, congratulations will be in order when you’ve achieved your goal. The sense of accomplishment you’ll feel at the end of your journey will truly make your home feel like a special place.

2. You Have Your Own Designated Happy Place

Owning your own home offers not only safety and security, but also a comfortable place where you can relax and unwind after a long day. Sometimes that’s just what you need to feel recharged and content.

3. You Can Find the Space To Meet Your Needs

Whether you want more room for your changing lifestyle (like retirement, dedicated space for a hobby, or a personal gym) or you simply prefer to have a large backyard for entertaining, you can invest in a home that truly works for your evolving needs.

4. You Can Customize Your Surroundings

Looking to try one of those decorative wall treatments you saw online? Tired of paying an additional pet deposit for your apartment building? Or maybe you want to create an in-home yoga studio. You can do all these things in your own home.

Whether you’re planning to purchase your first home or you’re ready to buy a different home to meet your needs, consider the emotional benefits that can turn a house into a happy home. When you’re ready to make a move, let’s connect.

The 2022 housing market has been defined by two key things: inflation and rapidly rising mortgage rates. And in many ways, it’s put the market into a reset position.

As the Federal Reserve (the Fed) made moves this year to try to lower inflation, mortgage rates more than doubled – something that’s never happened before in a calendar year. This had a cascading impact on buyer activity, the balance between supply and demand, and ultimately home prices. And as all those things changed, some buyers and sellers put their plans on hold and decided to wait until the market felt a bit more predictable.

But what does that mean for next year? What everyone really wants is more stability in the market in 2023. For that to happen we’ll need to see the Fed bring inflation down even more and keep it there. Here’s what housing market experts say we can expect next year.

Moving forward, experts agree it’s still going to be all about inflation. If inflation is high, mortgage rates will be as well. But if inflation continues to fall, mortgage rates will likely respond. While there may be early signs inflation is easing as we round out this year, we’re not out of the woods just yet. Inflation is still something to watch in 2023.

Right now, experts are factoring all of this into their mortgage rate forecasts for next year. And if we average those forecasts together, experts say we can expect rates to stabilize a bit more in 2023. Whether that’s between 5.5% and 6.5%, it’s hard for experts to say exactly where they’ll land. But based on the average of their projections, a more predictable rate is likely ahead (see chart below):

That means, we’ll start the year out about where we are right now. But we could see rates tick down if inflation continues to drop. As Greg McBride, Chief Financial Analyst at Bankrate, explains:

“. . . mortgage rates could pull back meaningfully next year if inflation pressures ease.”

In the meantime, expect some volatility as rates will likely fluctuate in the weeks ahead. If we see inflation come back under control, that would be good news for the housing market.

Homes prices will always be defined by supply and demand. The more buyers and fewer homes there are on the market, the more home prices will rise. And that’s exactly what we saw during the pandemic.

But this year, things changed. We’ve seen home prices moderate and housing supply grow as buyer demand pulled back due to higher mortgage rates. The level of moderation has varied by local area – with the biggest changes happening in overheated markets. But do experts think that will continue?

The graph below shows the latest home price forecasts for 2023. As the different colored bars indicate, some experts are saying home prices will appreciate next year, and others are saying home prices will come down. But again, if we take the average of all the forecasts (shown in green), we can get a feel for what 2023 may hold.

The truth is probably somewhere in the middle. That means nationally, we’ll likely see relatively flat or neutral appreciation in 2023. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“After a big boom over the past two years, there will essentially be no change nationally . . . Half of the country may experience small price gains, while the other half may see slight price declines.”

The 2023 housing market is going to be defined by mortgage rates, and rates will be determined by what happens with inflation. The best way to keep a pulse on what experts are projecting for next year is to lean on a trusted real estate advisor. Let’s connect.

This is normal.

This is bold.

Italics baby.

No matter what, be yourself.

If you’re a homeowner, your net worth got a big boost over the past few years thanks to rapidly rising home prices. Here’s how it happened and what it means for you, even as the market moderates.

Equity is the current value of your home minus what you owe on the loan.

Because there was a significant imbalance between the number of homes available for sale and the number of buyers looking to make a purchase over the past few years, home prices appreciated substantially.

And while home price appreciation has moderated this year, and even depreciated slightly in some overheated markets, that doesn’t mean you’ve lost all the equity you gained during the pandemic frenzy.

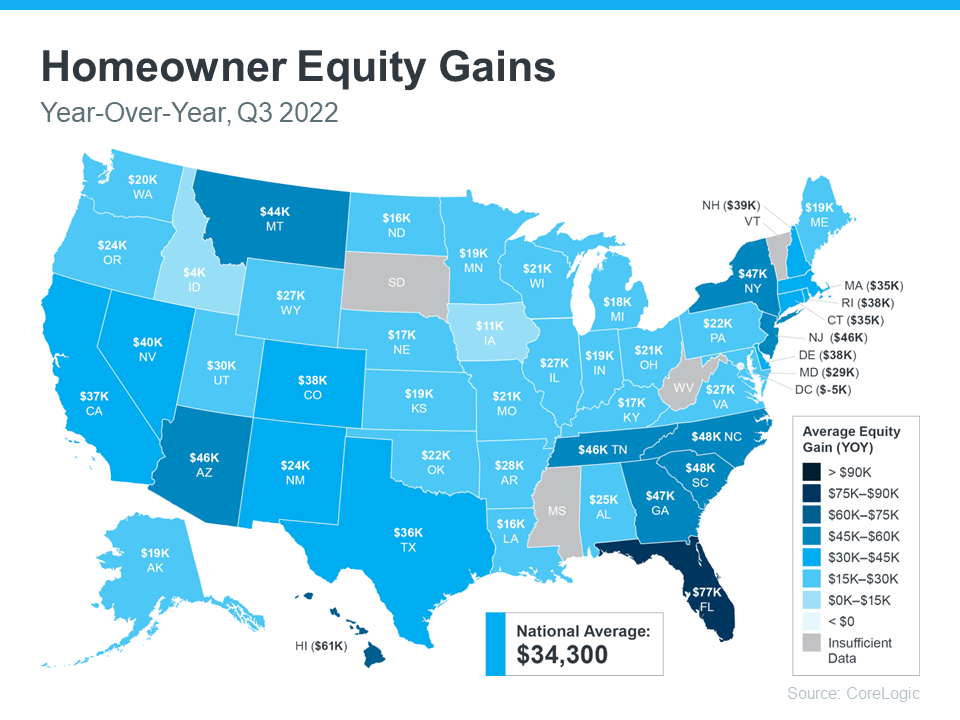

To prove you still have equity you can use, the latest Homeowner Equity Insights from CoreLogic finds the average homeowner equity has actually grown by $34,300 over the past 12 months.

That’s right, despite the headlines, the average homeowner still gained positive equity over the last year in just about every market. While the gains aren’t as dramatic as they were in the previous quarter due to home price moderation, they’re still significant. And if you’ve been in your home for longer than a year, chances are you have even more equity than you realize.

While that’s the national number, if you want to know what happened over the past year in your area, look at the map below from CoreLogic:

While equity helps increase your overall net worth, it can also help you achieve other goals, like buying your next home. When you sell your current house, the equity you’ve built up comes back to you in the sale, and it may be just what you need to cover a large portion – if not all – of the down payment on your next home.

So, if you’ve been holding off on selling because you weren’t sure what the headlines meant for your bottom line, rest assured you’ve still gained equity in recent years, and it can help fuel your move.

If you’re planning to make a move, the equity you’ve gained over time can make a big impact. To find out just how much equity you have in your current home and how you can use it to fuel your next purchase, let’s connect.

Mortgage rates have been a hot topic in the housing market over the past 12 months. Compared to the beginning of 2022, rates have risen dramatically. Now they’re dropping, and that has to do with everything happening in the economy.

Nadia Evangelou, Senior Economist and Director of Forecasting at the National Association of Realtors (NAR), explains it well by saying:

“Mortgage rates dropped even further this week as two main factors affecting today’s mortgage market became more favorable. Inflation continued to ease while the Federal Reserve switched to a smaller interest rate hike. As a result, according to Freddie Mac, the 30-year fixed mortgage rate fell to 6.31% from 6.33% the previous week.”

So, what does that mean for your homeownership plans? As mortgage rates fluctuate, they impact your purchasing power by influencing the cost of buying a home. Even a small dip can help boost your purchasing power. Here’s how it works.

The median-priced home according to the National Association of Realtors (NAR) is $379,100. So, let’s assume you want to buy a $400,000 home. If you’re trying to shop at that price point and keep your monthly payment about $2,500-2,600 or below, here’s how your purchasing power can change as mortgage rates move up or down (see chart below). The red shows payments above that threshold and the green indicates a payment within your target range.

This goes to show, even a small quarter-point change in mortgage rates can impact your monthly mortgage payment. That’s why it’s important to work with a trusted real estate professional who follows what the experts are projecting for mortgage rates for the days, months, and year ahead.

Mortgage rates are likely to fluctuate depending on what happens with inflation moving forward, but they have dropped slightly in recent weeks. If a 7% rate was too high for you, it may be time to contact a lender to see if the current rate is more in line with your goal for a monthly housing expense.