![Waiting To Buy a Home Could Cost You [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2021/07/29150309/20210730-KCM-Share-549x300.png)

![Waiting To Buy a Home Could Cost You [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2021/07/29150304/20210723-MEM-1.png)

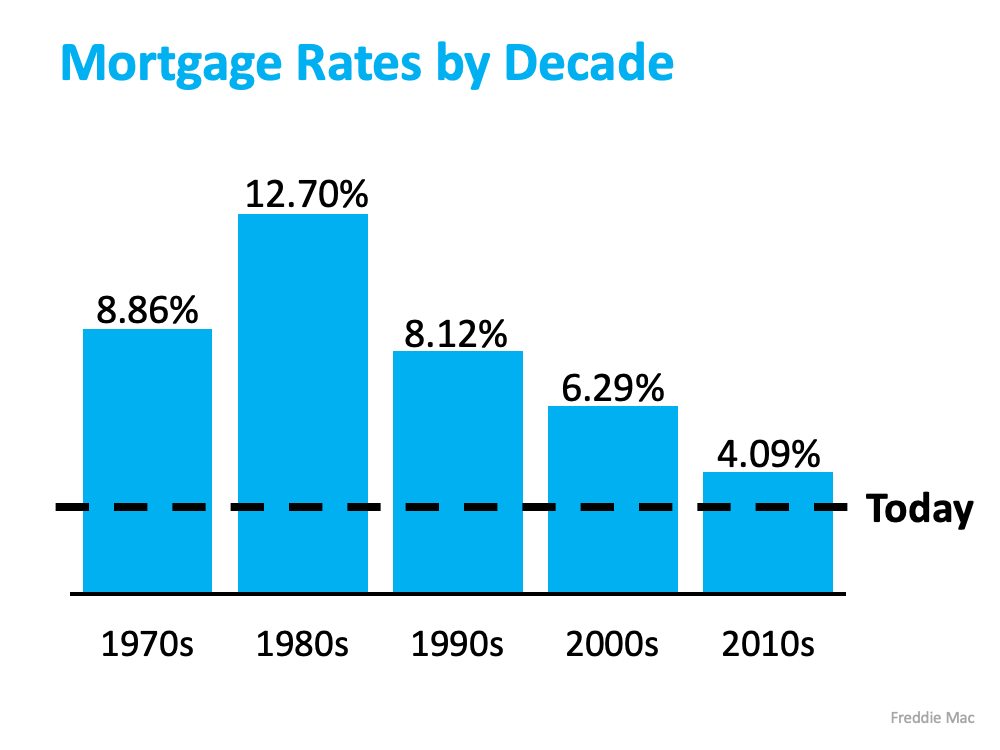

Some Highlights

- If you’re thinking of buying a home but wondering if waiting a few years will save you in the long run, think again.

- The longer the wait, the more you’ll pay, especially when mortgage rates and home prices rise. Even the slightest change in the mortgage rate can have a big impact on your buying power no matter your price point.

- Don’t assume waiting will save you money. Let’s connect to set the ball into motion today while mortgage rates are hovering near historic lows.

![Pop Quiz: Can You Define These Key Terms in Today’s Housing Market? [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2021/07/22135655/20210723-KCM-Share-549x300.png)

![Pop Quiz: Can You Define These Key Terms in Today’s Housing Market? [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2021/07/22135657/20210723-MEM.png)