![Is Right Now the Right Time to Sell? [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2021/01/28105016/20210129-KCM-Share-549x300.png)

![Is Right Now the Right Time to Sell? [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2021/01/28105012/20210129-MEM.png)

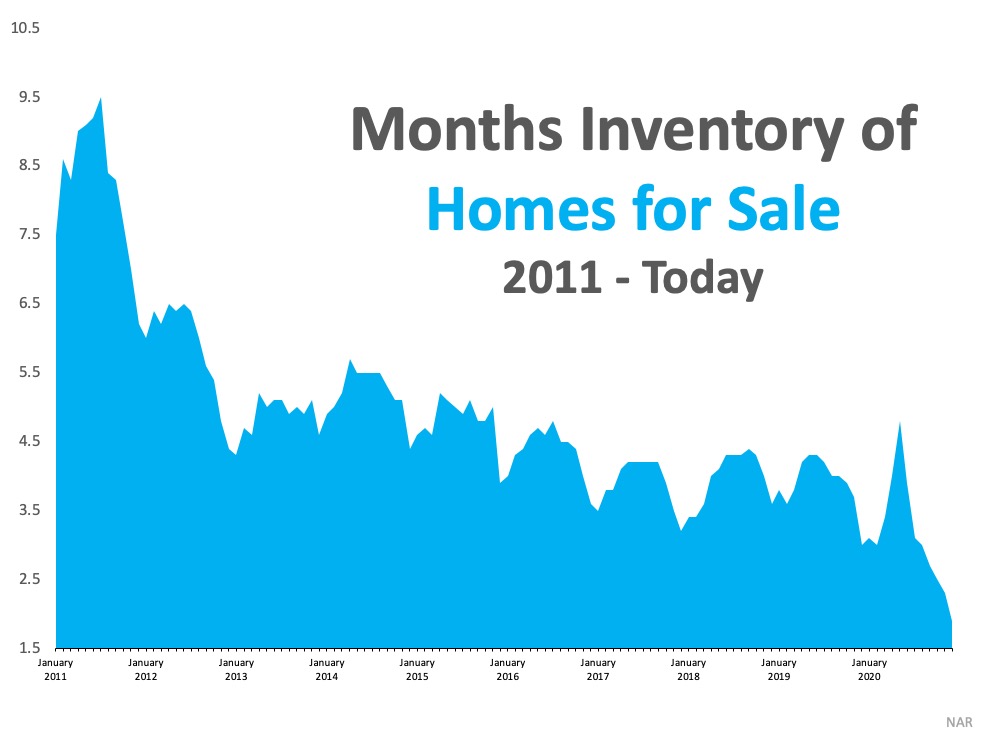

Some Highlights

- If you’re on the fence about selling your house, now is a great time to take advantage of sky-high demand, low supply, and fierce buyer competition.

- With buyer demand rising and historically low inventory for sale, if you’re in a position to move, your house may really stand out from the crowd.

- Let’s connect today to get your homebuying process underway.

![Financial Fundamentals for Homebuyers [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2021/01/21112615/20210122-KCM-Share-549x300.png)

![Financial Fundamentals for Homebuyers [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2021/01/21112610/20210122-MEM.png)